Visit to the WIIW

The Vienna Institute for International Economic Studies

The WIIW is one of the principle centres for research on Central, East and South-eastern Europe with 40 years of experience. Its thematic work is focused on macroeconomic developments and structural change, international economics, labour markets and social issues, as well as on selected issues related to sectoral and regional economic developments. It is an independent, non-profit institution with an international staff of highly skilled multilingual professionals with an intimate knowledge of the region.

Presentations:

1. WIIW Director of Research Michael Landesmann:

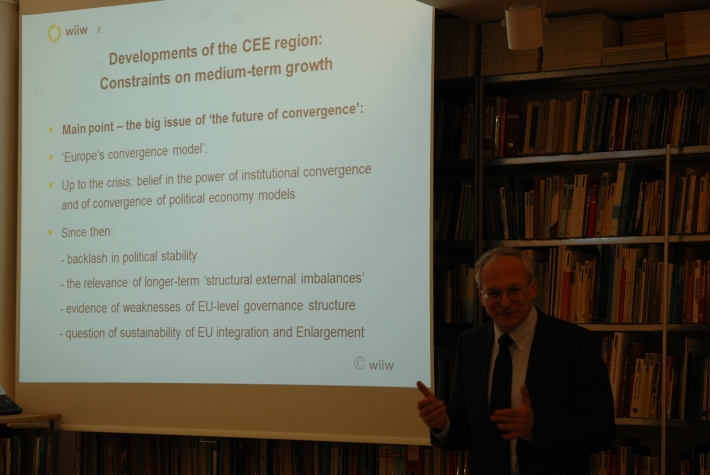

"Developments of the CEE Region"

2. WIIW Economist Vasily Astrov:

"Current Developments in the Ukraine from an Economic Perspective"

3. UniCredit Bank Austria CEE Strategic Analyst Mauro Giorgio Marrano:

"Banking in CEE - At the onset of a credit revival?"

In his speech, Director Landesmann pointed to the big issue of the future of convergence theory. Up to the crisis there was belief in the power of institutional convergence and of the convergence of political economy models. Since the crisis in 2008/2009 a severe reduction in political stability, an increase in the relevance of longe-term structural external imbalances, evidence of weakness in the EU-level governance structure and the question of sustainability of EU integration and enlargement can be observed. In many countries on Europe's Periphery, industrial production has suffered severely during the crisis. In his opinion, adjustment of current account is, in quite a few countries, mainly import-driven, real exchange rate developments have taken place due to quantity adjustments (especially employment contraction) and the corporate sector debt and banking sector problems have exerted a dampening impact on investment activity along with the withdrawal of capital.

Director Landesmann expects the debt legacy to continue to plague part of Europe's periphery for some considerable time, with a shift towards the trade sector quite diverse in this periphery. Agglomeration tendencies in manufacturing activity are very strong, a higher dispersion of industrial activity in the post-crisis period is questionable.

Economist Vasily Astrov, presenting current developments in the Ukraine, pointed out the country's very low GDP level, the lowest in Europe after Moldova. He emphasized the old production facilities with extremely high energy consumption. According to his opinion, the issue of Tymoshenko being held in prison for an unfavourable gas contract has been held as an obstacle to the initialling of the Association Agreement for too long. Later on, the economic aspect has become more important as the Ukraine should have adopted a large part of the Acquis Communautaire to help the country become more competitive through higher technical standards, public procurement regulations, an improvement of production processes etc. However, as there has been no definitive promise of full membership of the EU, the Russian political strategy of carrot and stick has worked. Ukrainian machinery and other fabricated products are exported to Russia because they can not be sold to EU-Countries. Now Russia has offered lower gas prices and a 15 Billion USD programme of purchasing Ukrainian Government Bonds with a 5% interest rate. When President Janukovych decided not to initial the Agreement he miscalculated the reaction of the protesters and allowed brutal attacks on them. The opposition has little influence on the protesters. President Janukovych may need to step down. Behind all this there is also the danger of a split of the country.

Strategic Analyst of UniCredit, Giorgio Marrano, drew a more positive picture of the short term developments in CEE. A recovery may be ahead of us. Concerning CEE Banking he expects a credit revival in a new model. CEE lending growth is rebounding with deposit growth at a comfortable level as part of a gradual adjustment process toward a more sustainable funding structure. Banks are experiencing and relying more on a much higher share of local deposits. This is supportive for the building up of a new model. However, asset quality is still a major downside risk factor to the scenario. For 2014 a gradual improvement is expected. Regulatory actions should lead to a better harmonization across the Region. He points out that notwithstanding several challenges the CEE banking sector remains profitable and shows much higher profitability than major WE countries. The gradual improvement in economic activity in the Region is likely to be accompanied by an acceleration of lending growth. Unicredit maintains a leadership position in CEE followed by Erste Bank and Raiffeisen Bank.

The presentations were followed by an extensive Q&A session.

Please find the presentatons in our download section (members only)